Key Points

- Strong Growth in Q1 2024: 11 out of 12 listed STAR Market semiconductor equipment companies reported positive year-over-year revenue growth, driven by surging AI demand and domestic efforts.

- Leading Performers: Beijing ZEON Corporation (京仪装备) saw the fastest revenue growth (54.23% YoY), while giants like AMEC (中微公司) and ACM Research (盛美上海) posted solid revenue and significant profit increases (ACM Research net profit up 207.21% YoY).

- Increased R&D Spending: Many companies are heavily investing in Research & Development, particularly for advanced processes (e.g., sub-12nm). This can sometimes impact immediate profitability but is crucial for maintaining technological leadership, as noted by CITIC Securities (中信证券).

- Policy and AI Tailwinds: Strong government support through initiatives like Big Fund III (allocating 30% to equipment/components) and accelerating demand from Advanced Packaging and AI are expected to fuel continued market expansion, with SEMI predicting significant global growth towards $121 billion USD in 2025.

Major players in China’s STAR Market semiconductor equipment sector are showing dynamic shifts, largely driven by surging AI demand and a national push for tech self-sufficiency.

As we dive into the Q1 2024 earnings and 2023 annual reports from these key tech companies, a clear picture emerges: while some are riding a wave of impressive growth, others are navigating profitability headwinds, often due to heavy R&D investment.

Let’s break down the latest performance data for these crucial players in the global semiconductor supply chain.

Find Top Talent on China's Leading Networks

- Post Across China's Job Sites from $299 / role

- Qualified Applicant Bundles

- One Central Candidate Hub

Your First Job Post Use Checkout Code 'Fresh20'

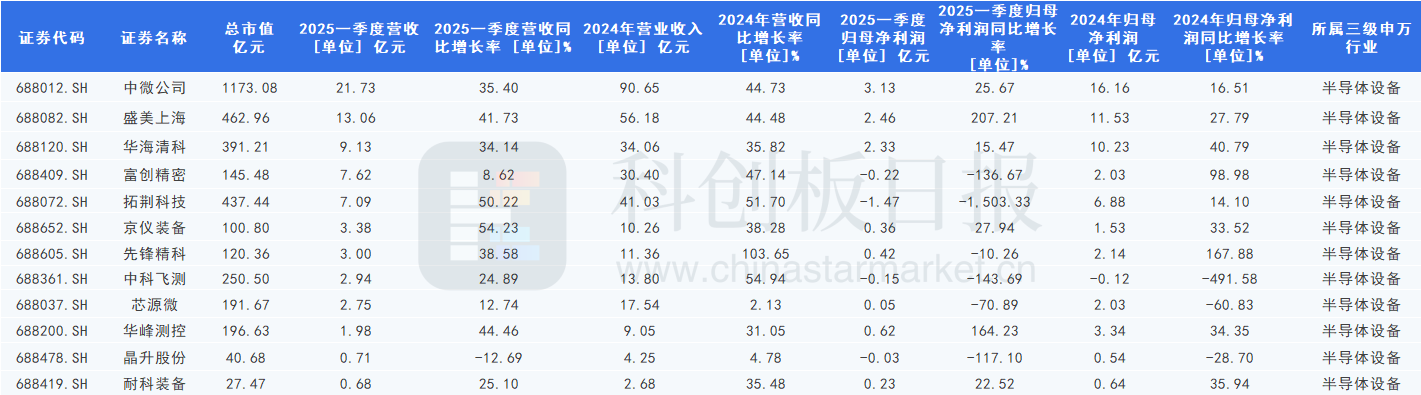

11 Out of 12 STAR Market Semi Equipment Companies Nail Positive Q1 Revenue Growth

The numbers don’t lie. Based on Cailianshe’s StarMine data (via Shenwan industry classifications), the semiconductor equipment landscape on the STAR Market is buzzing.

This sector covers critical areas like:

- Etching equipment

- Thin film deposition

- Testing equipment

- Cleaning equipment

In Q1 2024, an impressive 11 out of the 12 listed semiconductor equipment companies reported positive year-over-year revenue growth.

Here’s the growth ranking for Q1 2024:

- Beijing ZEON Corporation (Jingyi Zhuangbei 京仪装备)

- Piotech Inc. (Tuojing Keji 拓荆科技)

- AccoTEST (Huafeng Cekong 华峰测控)

- ACM Research (Shanghai), Inc. (Shengmei Shanghai 盛美上海)

- Zhejiang Jingsheng Mechanical & Electrical Co., Ltd. (Jingsheng Jidian 晶盛机电)

- Advanced Micro-Fabrication Equipment Inc. China (AMEC) (Zhongwei Gongsi 中微公司)

- Hwatsing Technology Co., Ltd. (Huahai Qingke 华海清科)

- Anhui NXET Co., Ltd. (Naike Zhuangbei 耐科装备)

- Skyverse Technology Co., Ltd. (Zhongke Feice 中科飞测)

- Kingsemi Co., Ltd. (Xinyuan Wei 芯源微)

- FS Precision Co., Ltd. (Fuchuang Jingmi 富创精密)

Only Jiangsu JGS-GW Electronics Co., Ltd. (Jingsheng Gufen 晶升股份) saw negative revenue growth during this period.

Q1 2024 YoY Revenue Growth Leaders

Source: Article data based on Cailianshe/StarMine.

ExpatInvest China

Grow Your RMB in China:

- Invest Your RMB Locally

- Buy & Sell Online in CN¥

- No Lock-In Periods

- English Service & Data

- Start with Only ¥1,000

Leading the charge was Beijing ZEON Corporation (Jingyi Zhuangbei 京仪装备).

They pulled in ¥338 million RMB ($46.6 million USD) in Q1, a hefty ¥119 million RMB ($16.4 million USD) jump from last year.

That’s a 54.23% year-over-year increase, marking three straight years of growth.

The company credits strong demand in the semiconductor equipment market and the competitiveness of its products.

Interestingly, this high growth coincided with a massive R&D push.

Beijing ZEON invested ¥94.1494 million RMB ($12.99 million USD) in R&D in 2023, up 53.06% year-over-year.

This boosted their R&D spending to 9.17% of operating revenue.

Another heavyweight, Advanced Micro-Fabrication Equipment Inc. China (AMEC) (Zhongwei Gongsi 中微公司), also posted strong Q1 numbers.

Revenue hit ¥2.173 billion RMB ($299.7 million USD), up 35.4% YoY.

Net profit followed suit, reaching ¥313 million RMB ($43.2 million USD), a 25.7% YoY increase.

AMEC is gaining serious ground, especially in etching equipment for sub-5nm processes in logic and memory chips.

Their 2023 annual revenue of ¥9.065 billion RMB ($1.25 billion USD) is already close to 15% of the revenue scale of similar lines from giant Applied Materials (Yingyong Cailiao 应用材料), signalling a major acceleration in China’s semiconductor localization efforts.

Resume Captain

Your AI Career Toolkit:

- AI Resume Optimization

- Custom Cover Letters

- LinkedIn Profile Boost

- Interview Question Prep

- Salary Negotiation Agent

Mixed Bag: Sub-Sector Performance Shows Differentiation

Digging deeper, the financial picture varies across different equipment types.

Take thin film deposition and measurement/inspection equipment – performance here is more nuanced.

Piotech Inc. (Tuojing Keji 拓荆科技), despite posting a Q1 net loss of ¥147 million RMB ($20.3 million USD), saw its revenue soar.

They brought in ¥709 million RMB ($97.8 million USD), a 50.22% YoY increase, second only to Beijing ZEON.

This points to the continued high demand in the thin film deposition market.

Chen Xinyi, GM of Piotech’s ALD Business Unit, highlighted at SEMICON China 2024 that the company leads domestically in ALD (Atomic Layer Deposition) equipment installations and process coverage.

Nearly 70% of their Q1 equipment sales revenue came from new products and processes.

So, why the loss? The company points to increased R&D investment in advanced process equipment below 12nm.

In the measurement and inspection space, Skyverse Technology Co., Ltd. (Zhongke Feice 中科飞测) reported Q1 revenue of ¥294 million RMB ($40.6 million USD), up 24.9% YoY.

However, their net loss widened to ¥15 million RMB ($2.07 million USD).

This is partly blamed on longer verification cycles for their equipment in memory wafer fabs.

Industry insiders suggest this “revenue up, profit down” scenario reflects the heavy upfront investment needed for high-end R&D.

The bet is that once customer certification is achieved, performance could see a significant turnaround.

On the other end, Jiangsu JGS-GW Electronics Co., Ltd. (Jingsheng Gufen 晶升股份) faced pressure on both top and bottom lines.

Q1 revenue was ¥70.8135 million RMB ($9.77 million USD), down 12.69% YoY.

Net profit attributable to the parent company was negative ¥2.5332 million RMB (-$0.35 million USD), a 117.10% YoY decrease.

Analysts at Huatai Securities (Huatai Zhengquan 华泰证券) attribute the revenue dip to price cuts in the downstream EV sector and inventory clear-outs in photovoltaics.

Profitability was further squeezed by depreciation from new production lines and increased R&D for new ventures.

Looking Back: 2023 Growth Trends Carry Momentum into 2024

The Q1 2024 results often mirror the momentum from 2023.

For the full year 2023, the standout revenue growth leaders were:

- Zhejiang Jingsheng Mechanical & Electrical Co., Ltd. (Jingsheng Jidian 晶盛机电) (Over 100% YoY growth!)

- Skyverse Technology Co., Ltd. (Zhongke Feice 中科飞测) (Over 50% YoY growth)

- Piotech Inc. (Tuojing Keji 拓荆科技) (Over 50% YoY growth)

- FS Precision Co., Ltd. (Fuchuang Jingmi 富创精密)

- Advanced Micro-Fabrication Equipment Inc. China (AMEC) (Zhongwei Gongsi 中微公司)

Comparing the full year 2023 and Q1 2024 figures shows that most companies continued their growth trajectory.

This suggests improving market demand and significant growth potential moving forward.

Investing in the Future: R&D Spend Ramps Up Across the Board

While overall revenue grew strongly, Q1 2024 net profits showed significant divergence.

In 2023, 9 companies saw positive YoY net profit growth, with only 1 reporting a loss.

However, in Q1 2024, only 6 companies boosted net profit YoY, while 4 reported losses.

Among the profit leaders, ACM Research (Shanghai), Inc. (Shengmei Shanghai 盛美上海) stood out.

Their Q1 2024 net profit attributable to the parent company hit ¥246 million RMB ($33.9 million USD), a massive 207.21% YoY surge.

ACM Research attributes this to the recovering global semiconductor industry, particularly strong demand in mainland China, and a healthy backlog of orders.

Chairman Dr. David Wang (Wang Hui 王晖) recently stated their wet processing equipment now holds over 25% market share in China’s logic chip market.

AMEC (Zhongwei Gongsi 中微公司), the STAR Market’s largest semi equipment firm by market cap and revenue, also saw solid profit growth.

Q1 net profit reached ¥313 million RMB ($43.2 million USD), up 25.67% YoY.

AMEC reported significant shipment increases for high-end etching products in Q1, achieving mass production for critical processes in advanced logic and memory devices.

They’ve also successfully launched six types of thin film deposition equipment and moved EPI equipment into client-side mass production verification.

Overall, the leading players like AMEC, ACM Research, and Hwatsing Technology Co., Ltd. (Huahai Qingke 华海清科) are driving the industry’s profitability.

Meanwhile, companies like Skyverse Technology (Zhongke Feice 中科飞测) and FS Precision Co., Ltd. (Fuchuang Jingmi 富创精密) slipped into losses, often due to capacity pre-builds and heavy R&D spending.

For instance, FS Precision Co., Ltd. (Fuchuang Jingmi 富创精密) reported a Q1 loss of ¥22.1569 million RMB ($3.06 million USD).

Yet, their R&D expenses in the same period were ¥54.70 million RMB ($7.54 million USD), up 16.26% YoY.

The company explicitly cited capacity pre-investment, talent acquisition, and R&D input as factors behind the loss.

Even Jiangsu JGS-GW Electronics Co., Ltd. (Jingsheng Gufen 晶升股份), which saw revenue grow only 4.78% and net profit drop 28.7% in 2023, increased its R&D investment.

Their 2023 R&D spend reached ¥44.2471 million RMB ($6.10 million USD), up 16.39% YoY and representing 10.41% of annual revenue.

As Wang Zhe, an analyst at CITIC Securities (Zhongxin Zhengquan 中信证券), notes: “the R&D cycle for semiconductor equipment is as long as 3 to 5 years and requires continuous investment to maintain technological leadership, which places higher demands on corporate cash flow management capabilities.”

Tailwinds: AI Demand and Policy Fuel Semiconductor Equipment Market Optimism

The broader market context is positive.

According to the semiconductor industry association SEMI, global semiconductor equipment sales hit a record $107.6 billion USD in 2022, followed by $106.3 billion USD in 2023, marking the second consecutive year above $100 billion. (Note: The original data source mentioned different figures for 2022/2023 potentially reflecting regional data or projections, but official SEMI figures confirm the strong market).

SEMI forecasts the global market could reach $121.0 billion USD in 2025.

Crucially, China’s mainland expansion is accelerating, positioning it to lead the global market.

Ajit Manocha, President and CEO of SEMI, emphasized China’s role as the largest downstream market.

Projections suggest China’s semiconductor equipment market size could reach $45.0 billion USD (potentially a future year estimate, as 2023 was ~$30B according to SEMI), with over $100 billion USD in investments planned over the next three years.

What’s driving this growth?

- Advanced packaging technology

- Emerging applications like