Key Points

- Multiple Chinese private banks, including Zhongguancun Bank (Zhongguancun Yinhang 中关村银行), are suspending or removing 3-year and 5-year fixed deposit products, indicating a strategic retreat from high-interest, long-term liabilities.

- This trend is driven by a shrinking Net Interest Margin (NIM), which has declined by 0.77 percentage points since the end of 2023 for private banks, making high-cost deposits unsustainable.

- Banks face a lending problem, with falling loan yields and negative loan growth for 7 out of 18 reporting private banks in 2025, reducing the need for expensive long-term funding.

- Some banks are experiencing interest rate inversion, where shorter-term deposits offer higher rates (e.g., Hunan Sanxiang Bank’s 2-year at 2.0% vs. 3-year at 1.95%), indicating a push to shorten liability maturity.

- The move signifies a broader shift for Chinese private banks to focus on risk control, customer acquisition, and specialized sectors rather than competing solely on high deposit rates.

- Lower overall funding costs to protect Net Interest Margins (NIM)

- Enhance flexibility to respond to future benchmark rate adjustments

- Improve asset-liability maturity matching amid falling loan yields

- Shift competitive focus from price wars to specialized financial services

Something’s shifting in China’s banking landscape.

Multiple private banks across the country are making a strategic retreat from their most attractive deposit products.

Instead of offering competitive long-term fixed deposits, they’re suspending or removing 3-year and 5-year options entirely.

And the reason why reveals a lot about the current state of Chinese finance.

The Great Deposit Pullback: Which Banks Are Doing It

Let’s start with what’s actually happening on the ground.

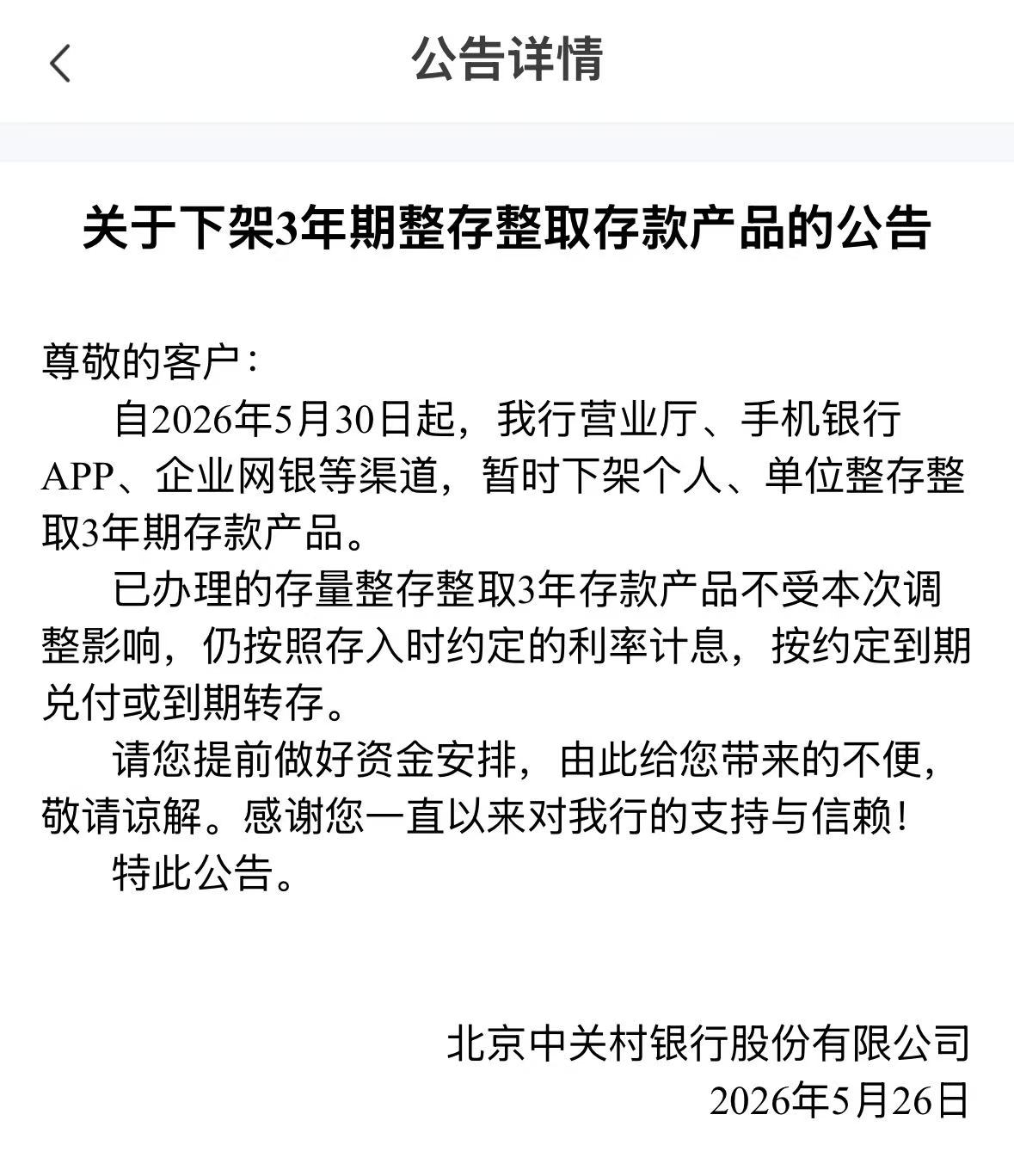

Zhongguancun Bank (Zhongguancun Yinhang 中关村银行) kicked things off by announcing in May that it would temporarily suspend 3-year fixed deposit products for both individual and corporate clients.

But here’s the thing—they’re not alone.

A review of private bank apps across China reveals that a wave of institutions have disabled or removed long-term deposit options:

- Jilin Yilian Bank (Jilin Yilian Yinhang 吉林亿联银行)

- Blue Ocean Bank (Weihai Lanhai Yinhang 威海蓝海银行)

- Hunan Sanxiang Bank (Hunan Sanxiang Yinhang 湖南三湘银行)

- MYbank (Zhejiang Wangshang Yinhang 浙江网商银行)

- Huahui Bank (Shanghai Huaru Yinhang 上海华瑞银行)

- Jiangsu SuShang Bank (Jiangsu Sushang Yinhang 江苏苏商银行)

Some banks show 5-year products as “Sold Out.”

Others have removed the listings entirely.

Find Top Talent on China's Leading Networks

- Post Across China's Job Sites from $299 / role

- Qualified Applicant Bundles

- One Central Candidate Hub

Your First Job Post Use Checkout Code 'Fresh20'

ExpatInvest China

Grow Your RMB in China:

- Invest Your RMB Locally

- Buy & Sell Online in CN¥

- No Lock-In Periods

- English Service & Data

- Start with Only ¥1,000

What Zhongguancun Bank Actually Did (And Why It Matters)

Let’s break down Zhongguancun Bank’s specific move, because it’s the clearest example of this trend.

Starting May 30, the bank suspended 3-year Lump-sum Deposit and Withdrawal products across:

- Physical bank branches

- Mobile banking app

- Corporate online banking channels

Important note: Existing 3-year deposits customers already have aren’t affected.

They’ll continue earning interest at their agreed-upon rate until maturity or rollover.

This is a new customer suspension, not a retroactive policy change.

Resume Captain

Your AI Career Toolkit:

- AI Resume Optimization

- Custom Cover Letters

- LinkedIn Profile Boost

- Interview Question Prep

- Salary Negotiation Agent

The Rate Decline Timeline

What makes this really interesting is the historical context.

Back in October 2025, Zhongguancun Bank had already lowered rates on several products:

- 2-year products: 1.8%

- 2-year new customer products: 1.9%

- 3-year products: 2.1%

- 5-year products: 2.0%

The 5-year product got removed in April 2024.

The 3-year product was taken down, brought back, then suspended again on May 30.

Now the bank’s app only shows:

- 2-year: 1.8% annual

- 1-year: 1.6% annual

- 6-month: 1.4% annual

- 3-month: 1.2% annual

Translation: all fixed deposit rates now fall into the “1% range.”

The Weird Rate Inversion Problem

Here’s where things get really strange.

Some banks are experiencing interest rate inversion—where shorter-term deposits pay more than longer-term ones.

Hunan Sanxiang Bank (Hunan Sanxiang Yinhang 湖南三湘银行) is a prime example:

- Their 2-year fixed deposit: 2.0%

- Their 3-year fixed deposit: 1.95%

Customers actually get less interest for locking up their money longer.

That’s backwards.

And it’s happening because banks need to shed themselves of high-cost, long-term liabilities.

Why This Is Actually Happening: The Net Interest Margin Crisis

Here’s the real story behind the headlines.

Chinese private banks are under serious margin pressure.

An insider from a private bank explained the thinking directly to reporters: “If we can’t issue enough loans, why would we want so many high-interest deposits?”

It’s a fair question.

The core problem: Shrinking Net Interest Margins (NIM).

NIM is the gap between what banks earn on loans and what they pay on deposits.

When that gap shrinks, profitability gets squeezed.

The Numbers Tell the Story

According to the National Financial Regulatory Administration (Guojia Jinrong Jiandu Guanli Zongju 国家金融监督管理总局), private bank NIM has been declining steadily:

- Q1 2026: 3.62% NIM

- End of 2025: Compared to Q1 2026, down 0.21 percentage points

- Since end of 2023: Cumulative decline of 0.77 percentage points

That’s a meaningful compression over just a couple years.

For context, that’s the difference between a healthy margin and a struggling one.

The Lending Problem

Here’s what’s driving the margin collapse: loan yields are falling.

When loan rates drop but deposit rates stay high, banks get crushed in the middle.

Some private banks have actually stopped growing their loan portfolios.

Data from late 2025 shows:

- 18 private banks published annual reports

- 7 of those 18 saw negative loan growth compared to 2024

Translation: roughly 39% of reporting private banks couldn’t grow their loan books in a meaningful way.

So why hold expensive, long-term deposits if you don’t have customers to lend them to?

What Industry Experts Are Saying

Jiang Han (Jiang Han 江瀚), a senior researcher at Pangu Institution (Pangu Zhiku 盘古智库), broke down the strategic thinking:

“The core driver is the macro pressure on NIM across the banking industry. With loan yields falling, maintaining high-cost long-term deposits would squeeze margins to the point of inversion. Banks must shorten the average maturity of their liabilities to remain flexible.”

In other words: by suspending long-term deposits, banks can:

- Reduce their interest payment obligations

- Lower their average liability costs

- Keep more flexibility for future rate cuts

- Avoid getting locked into high-cost funding at a time when lending opportunities are scarce

It’s a defensive move, not an offensive one.

The Bigger Picture: What’s Next for Chinese Private Banks

This deposit pullback signals something bigger happening in China’s banking sector.

According to industry analysts, private banks can’t rely on old playbooks anymore.

The growth-at-all-costs era is over.

What private banks need to focus on instead:

- Risk control: Ensuring asset quality, not just asset growth

- Customer acquisition: Building a stable, long-term customer base

- Specialized sectors: Like “Industrial Banking” or “Technology Finance” where they can compete on expertise, not just rates

A source from a city commercial bank summed it up bluntly:

“Banks that rely solely on high interest rates to attract deposits without a core competitive advantage or a solid base of fundamental customers will face significant challenges in the future.”

That’s the real warning here.

The days of using deposit rates as a competitive weapon are fading.

Banks that can’t differentiate beyond interest rates are going to struggle.

What Does This Mean for Depositors and Investors?

If you’ve got money in a Chinese private bank, here’s what to watch:

- Lower yields ahead: Expect deposit rates to keep declining as more banks reduce product offerings

- Shorter lock-up periods: Banks will increasingly push shorter-term deposits (6-month to 1-year) instead of 3-5 year products

- Competitive fragmentation: Banks with strong customer bases and specialized niches will hold rates better than those without

- Risk consideration: As margins compress, bank health becomes more important—not all private banks will survive without further consolidation or restructuring

For investors in banking stocks, this is a red flag about profitability headwinds.

For depositors, it’s a reminder that rates won’t stay attractive forever—lock in what you can while products are still available.

The Bottom Line on Chinese Private Banks and Fixed Deposits

What we’re seeing across Zhongguancun Bank (Zhongguancun Yinhang 中关村银行), Jilin Yilian Bank (Jilin Yilian Yinhang 吉林亿联银行) defender seven other private banks isn’t random.

It’s a coordinated retreat driven by real economic pressures:

- Shrinking profit margins (NIM down 0.77 percentage points since 2023)

- Falling loan yields with no way to profitably deploy deposits

- 39% of large private banks couldn’t grow loans in 2025

The playbook is changing.

Chinese private banks are moving away from being rate-driven commodity players and toward being specialized financial institutions with real competitive advantages.

If they can’t make that transition, the margin squeeze will get worse—and so will the pressure on deposit products.

For anyone monitoring Chinese financial markets, this shift in private bank strategy is one of the most important developments to understand right now.